Property has been a major source of wealth building over the last couple of decades. And has been the vehicle of choice for “Mum & Dad” investors.

But is this growth sustainable? And how does Property as an investment stack up against Shares in the medium to long term?

The answer to the first is while historically property prices have steadily increased, this is by no means guaranteed. Outside Sydney and Melbourne, property prices have fallen significantly in Perth by 10% as of 2017. And other capital city prices are likely to fall with the Federal Government urging regulators and banks to clamp down on lending.

And even if the falls aren’t major, capital growth has slowed.

To compare investing in property versus shares, let’s start by ensuring we measure apples with apples.

Most people analysing shares do so on a short term basis, usually daily. We consume stock reports in the media which point to shares going up or down (sometimes dramatically) every day. Consequently we have the impression shares are volatile.

Uniquely combining both Fundamental and Technical Analysis

Not yet a subscriber? Join now for FREE!

Receive our weekly tips and strategies into your inbox each week.

BONUS: Sign up now to download our 21 page Trading Guide.

While to some extent this is true, if we applied the same measurement criteria to housing prices, i.e. watched the market price of a specific house daily, we’d see large levels of fluctuation as well depending on whether someone wanted to buy/sell and on what terms.

According to ABS data, the median house price in Australia in 1996 was $143,921. In 2016 the median house price was $623,000. An overall gain of 332% or $479,079.

While this looks great on paper, what about the costs of maintaining the property over that time?

Comparatively, if you had a portfolio that tracked the All Ordinaries share index, and it was worth $143,921 in 1996, today it’d be worth $357,000. Now that’s also pretty good.

But, the cost of maintaining shares is virtually zero compared to typical costs of owning property, like stamp duty, council rates, body corporate fees, general maintenance and insurance, which are ongoing, and can run into the tens of thousands.

However, it can get much better.

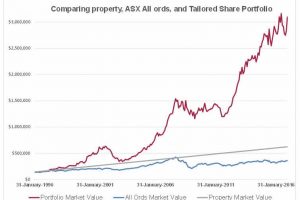

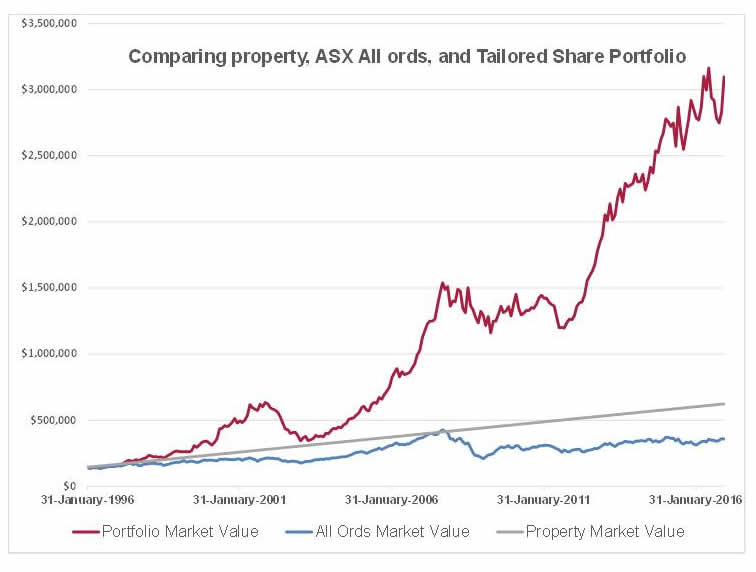

Say in 1996, you invested $143,921 in a portfolio and took some simple advice of only choosing a few of the biggest blue chip shares, and avoided the risky ones.

Imagine just picking 4 stocks, spread evenly between Commonwealth Bank, BHP, CSL, and Woolworths, which are all household names.

We know that BHP and Woolworths haven’t been doing too well recently so it’s a fair mix. Only 20 years later, at the end of 2016, that $143,921 would be worth $3.2m. This doesn’t include 20 years of dividends. Not a bad amount to now retire on.

So by being a little more selective with your shares, you have returned more than 2200% compared to a 332% gain in property.

The graph below charts Property Verses Share growth over a 20 year period.

Capital growth aside, let’s look at other factors you should take into consideration.

Growth versus Income

Most property investors are looking for capital growth over time. Unless the asset is positively geared (becoming a rarity in major capital cities), you have to use your own income to keep paying for the asset which negatively impacts on your cash flow.

Given the cash flow demands, if negatively geared, there is a limit to how many properties you can invest in as you’d run out of cash.

Good quality Shares on the other hand can provide significant dividend income regardless of the current stock price, provided that the company is maintaining its earnings.

Shares also attract franking credits of up to 30% for tax already paid by the company. If you ordinarily don’t pay any tax (as a retiree), then you can receive tax back, adding to your annual income. For example, if you receive a 5% dividend on a stock that is fully franked, then you can receive an additional 2.14% (or a total of 7.14%) on your money.

Investment Timeframes

Corelogic research shows that homes resold that resold at a loss had a typical length of ownership of 6.1 years for houses and 6.5 years for units.

To achieve a gross profit, the typical length of ownership was recorded at 9.1 years for houses and 7.6 years for units. Which means your money is tied up for years. And should property prices fall (as they have in Perth and a number of mining towns in WA), it’s very difficult to cut your losses and sell. After all, who’s going to buy a property when there’s no prospect of upward movement?

So if investing in property, be prepared for the long haul. But many investors buying now expect to be ahead from day one, as if property prices are a runaway steam train.

Price rises have also seen yields drop to very low levels. Gross yields in Sydney now sits at 2.8% for houses and 3.8% for units.

At time of writing, Commonwealth Bank shares have a gross yield of 7% and Telstra is over 10%. If the share prices take a dip, then these yields become even greater.

Cost of Acquisition & And ongoing costs

Property:

While Banks require a minimum 5% cash deposit for investment properties, putting in at least 10% to 20% means you avoid the added costs of mortgage insurance.

Add in stamp duty, legal and loan establishment costs. In addition, if you use a buyer’s agent to help you source the property you’ll pay upwards of $8K to $10K. So all up, you’d be looking at $50K+ just to get started.

Then there are the ongoing costs of maintenance, insurance, mortgage payments, land tax, strata fees, council rates and utility bills.

Added up this means you need at least a 5% return to break even.

Shares:

You could start with as little as $1,000. But let’s compare apples with apples by investing $1M in shares.

An experienced broker who will help you create a portfolio and give personal advice will charge 1% of the stock price. For a $1M investment this equates to $10,000 once off. There are no ongoing fees to maintain these shares. And remember, depending on what you select, you’ll also receive dividend payments.

Investment Risk – Property versus Shares

While property prices have steadily risen over the last few years, sometimes spectacularly, the easy money has been made.

Property prices do fall. Perth prices are down 10% since their high in December 2014.

If you’d invested in a mining town during the boom, try getting rid of your property now at any price. While you still pay the mortgage!

With the Federal Government putting more and more pressure on regulators, APRA is imposing further constraints on interest only loans, banks raising rates out of cycle and large investment firms such as UBS are now calling a top in the market.

This is before we consider the politics of negative gearing which dominates the news every day.

Clearance rates are now softening and CoreLogic now say that in the month to 20 April, housing prices in the 5 largest cities increased only 0.3%.

The curve is now starting to flatten out.

So there is a risk that your property could fall in value. This means that by the time it rises again, you have spent plenty of years paying off a mortgage for nothing.

While Shares appear to be more volatile, you can diversify your portfolio to minimise risk. Shares are liquid assets so partnered with a professional advisor you can be nimble and take advantage of excellent buys.

Remember, money is always made on the way in. Buy low, sell high. A rare event in the property market today.

There are many things to like about property investments. Most people view it as a more “tangible asset” but that is taking a more emotional perspective. Unfortunately most people let their emotions guide their financial choices. In reality, property is not more secure than a company shareholding, and we know that stocks do have plenty of advantages over bricks and mortar.

To summarise, the key points are:

1. Shares are simple to invest in. You can easily start by just picking a few top index stocks which have solid companies behind them. The shares should be fairly stable in capital value and if you’re mainly looking for dividend income, this is an easy way to generate cash flow.

2. You have a liquid cash position. Shares are easy to buy and sell. You’ll get your money pretty much immediately.

Property is a fixed asset. If you need to sell in a hurry, depending on market conditions in that specific area, you might be up for a fire sale. Add in the normal 90 to 120 day settlement period, agent’s fees and other costs, you’re not only going to wait a while for your money, but lose a lot in the transaction. There’s also a lost opportunity cost while waiting for your cash.

3. Ease of purchase. You buy the shares at the quoted price. You can do it yourself via online portals. It’s location independent.

While you could buy property sight unseen, most won’t. So there are inspection costs, conveyancing, legal fees, agent fees, not to mention haggling with the vendor.

4. Portfolio Diversification. Investing is all about risk management and mitigation. Depending on your risk profile you can select a range of stocks to give you growth and income. You can hedge your bets by ensuring no more than 5% – 10% of your money is tied up in any one stock.

Try doing that with property.

5. Levels of debt. It’s highly unlikely you’ll buy decent property with your own cash. Ergo, you’ll need to go into high levels of debt to fund your investment. Fine while things are going up. But what when the price of your property falls below your mortgage level and the bank demands repayment? Yes, it does happen.

You can invest in stocks using your own money. A few thousand dollars will get you started.

6. Volatility is a distinct advantage. Every seasoned investor knows money is made on the way in. e. Buy low, sell high.

It’s very difficult to buy property at a “bargain” price and your strategy will be a buy and hold looking for long term capital growth. But remember to achieve a gross profit, the typical length of ownership was recorded at 9.1 years for houses and 7.6 years for units.

Shares rise and fall. With the right advice you can buy specific stocks at the bottom of a cycle and sell them quickly as the market tops out. You could achieve this in a matter of days, weeks or months. Naturally, we’d recommend getting professional advice on reading the cycle.

What’s next?

If you’re looking to invest in shares (and why wouldn’t you given the analysis above), we can help you make the right choices given your circumstances, risk profile and stage of life.

At Fairmont Equities, we offer a wide range of help from education aimed at beginning investors, all the way to done for you managed portfolio advice.

Start by downloading our free guide on how to improve your trading results by combining fundamental and technical analysis. It’s geared towards people wanting to dip a toe into share trading.

We also offer a fully researched Weekly Trading Report used by DIY traders around Australia who want the research done for them.

And of course, you can ask us to manage your portfolio for you. You can check out the various options here.